This article is featured in our Spring 2014 issue of the CER Journal.

Introduction

A dramatic portrait of Matsukata Masayoshi can be found in most typical Japanese histories. Rising to the office of Finance Minister in October 1881, he is seen as having inherited an economy on the brink of financial disaster. As one historian described the situation, the condition of the economy was “characterized by soaring quantities of paper currency unbacked by species” and “inevitable inflation,” along with other problems, which together implied “the end of dreams of national prosperity and international equality.”[1] During this crisis, Matsukata stood at the helm of the economy, faced with a difficult decision. He could pursue a policy of fiscal restraint, plunging the agricultural sector into a depression, or he could do nothing and risk the collapse of the fledgling economy—or so the usual narrative claims.

A dramatic portrait of Matsukata Masayoshi can be found in most typical Japanese histories. Rising to the office of Finance Minister in October 1881, he is seen as having inherited an economy on the brink of financial disaster. As one historian described the situation, the condition of the economy was “characterized by soaring quantities of paper currency unbacked by species” and “inevitable inflation,” along with other problems, which together implied “the end of dreams of national prosperity and international equality.”[1] During this crisis, Matsukata stood at the helm of the economy, faced with a difficult decision. He could pursue a policy of fiscal restraint, plunging the agricultural sector into a depression, or he could do nothing and risk the collapse of the fledgling economy—or so the usual narrative claims.

From this perspective, Matsukata’s financial reforms between 1881 and 1885 and the resulting deflationary period, referred to as the “Matsukata Deflation,” are often viewed as a heroic, yet costly, rescue of the Japanese economy. While this depiction of the Matsukata Deflation is not entirely inaccurate, it misrepresents the nature of Matsukata reforms by failing to take into account the circumstances and motivations of the policies. In context, it is clear that the Matsukata Deflation was not a response to any singular macroeconomic event in the Japanese economy, such as rising inflation, but rather was part of a general program, centered on the establishment of a convertible currency, with the goal of restructuring the financial system and ensuring the government’s financial security.

Long-term and Intermediate Objectives

At the outset of the Meiji Restoration, the new government was committed to the long-term objective of increasing Japan’s prosperity and power. To achieve this greater goal, the government had to create the conditions under which such growth could occur. In the view of government leaders, the key to success was financial reform, making the establishment of a sustainable financial policy an essential intermediate goal. Matsukata’s memorandum to the cabinet council in March 1882 reflected this view:

In national affairs, there is nothing of greater importance than a financial policy. The Prosperity of the nation, the happiness of the people, the awakening of industrial enterprises and the activity of commercial transaction, all are closely bound up with a sound financial policy of the country.[2]

The primary financial problems that needed to be addressed to promote growth included the interrelated issues of the government’s budget, the monetary system, including modern financial institutions, and the balance of payments. A sharp increase in domestic money supply, such as one caused by a government issuing new notes, frequently produces inflation, which will generate an increase of imports over exports. The effect is an outflow of specie, which interferes with the establishment of convertible currency. As this brief sketch of the relationship between these issues suggests, government expenditures and revenues play a key role in fulfilling the goals set out for Japan’s economy.

Historical Overview: Beginning of Meiji Restoration

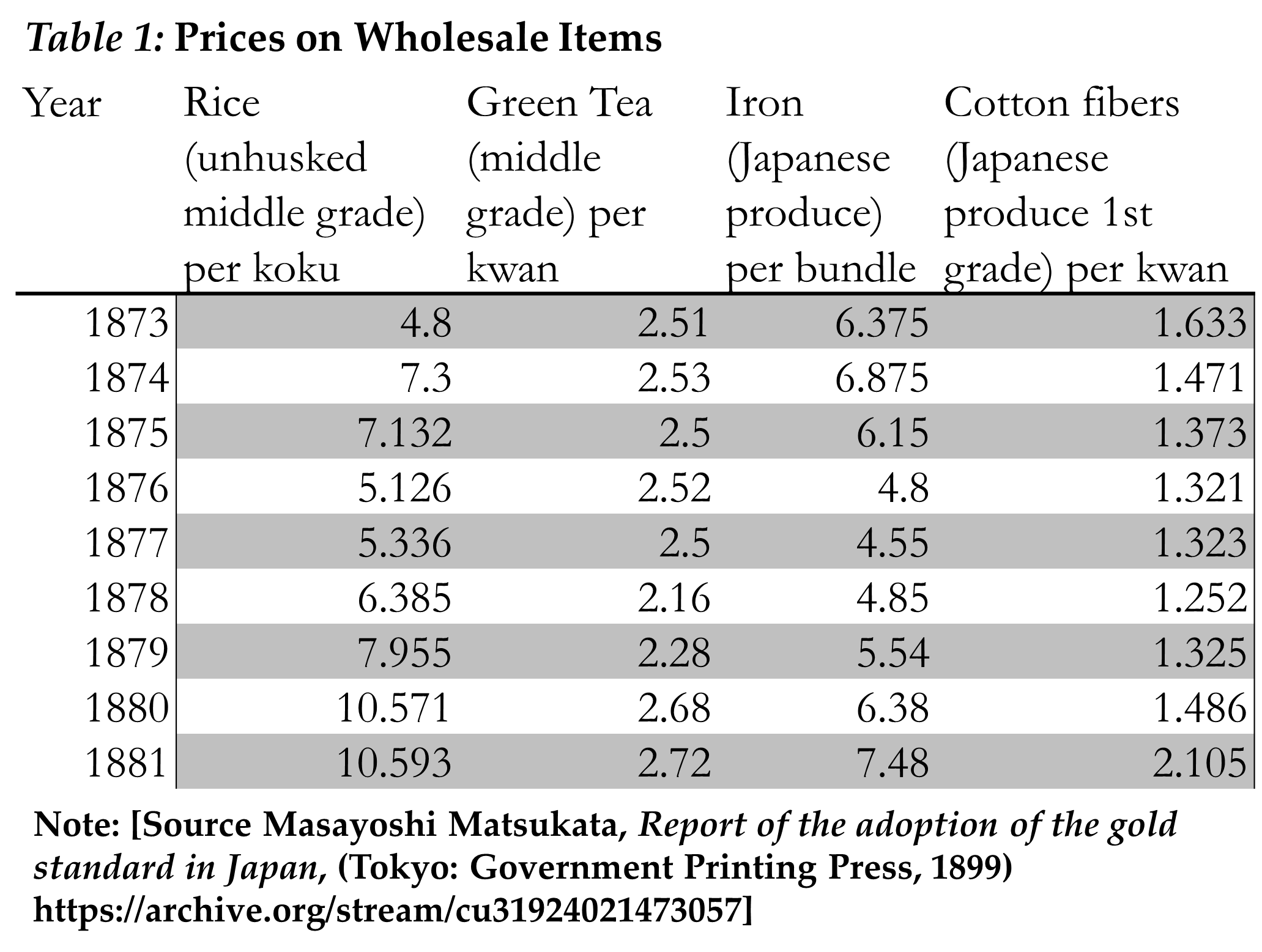

When the central government assumed power in 1868, it was immediately faced with a serious financial problem. It was not prepared to shoulder the heavy burdens left by the Tokugawa regime, and significant funds were needed to defeat Tokugawa loyalists, continue pension payments former samurai, and service the former government’s debts. The government also implemented other costly programs in the following years, including the modernization of the army and navy and the allocation of funds for subsidized enterprises and model factories. To meet these early deficits, the government issued new inconvertible notes that existed alongside previously established han currency. Between 1873 and 1875, the Meiji began to take larger steps toward advancing the economy through the implementation of a land tax, the redemption of paper money, and the formation of a national banking system. Paper note redemption was slow, since the government offered bonds in exchange which carried interest rates below market rates, and few National Banks were opened due to unprofitable restrictions placed on them.[3] Of these three policies, the land tax proved most important initially. Besides establishing private ownership of agricultural land, the 1873 chiso kaisei reform, which replaced the previous rice tax with a monetary land tax, provided the government large revenues.[4] Data on inflation during this period is limited, but available price data suggests little inflation occurred, keeping in mind the continuing process of adjustment of relative prices to world relative prices (Table 1).

Inflationary Period, 1876-1881

Two significant shocks hit the economy in 1876 and 1877, closely related in cause and complementary in effect. First, in 1876, the government instituted compulsory commutations of bushi stipends to former samurai. The stipends were replaced by bonds (kinroku kosai) amounting to a total of ¥172.9 million.[5] Soon after the capitalization of pensions followed the Satsuma rebellion, which required the government to borrow ¥15 million from the Fifteenth National Bank and print another ¥27 million.[6] According to Ōkuma Shigenobu, who was Minister of Finance at the time, the capitalization of pensions was intended to help former samurai find new employment and to stimulate the economy.[7] More immediately, the government benefited from the removal of a heavy transfer burden that had been consuming much of its budget. The percentage of the government’s yearly expenditures consumed by transfer payments fell to 35% from a height of 53% in 1875 (Fig. 1).[8]

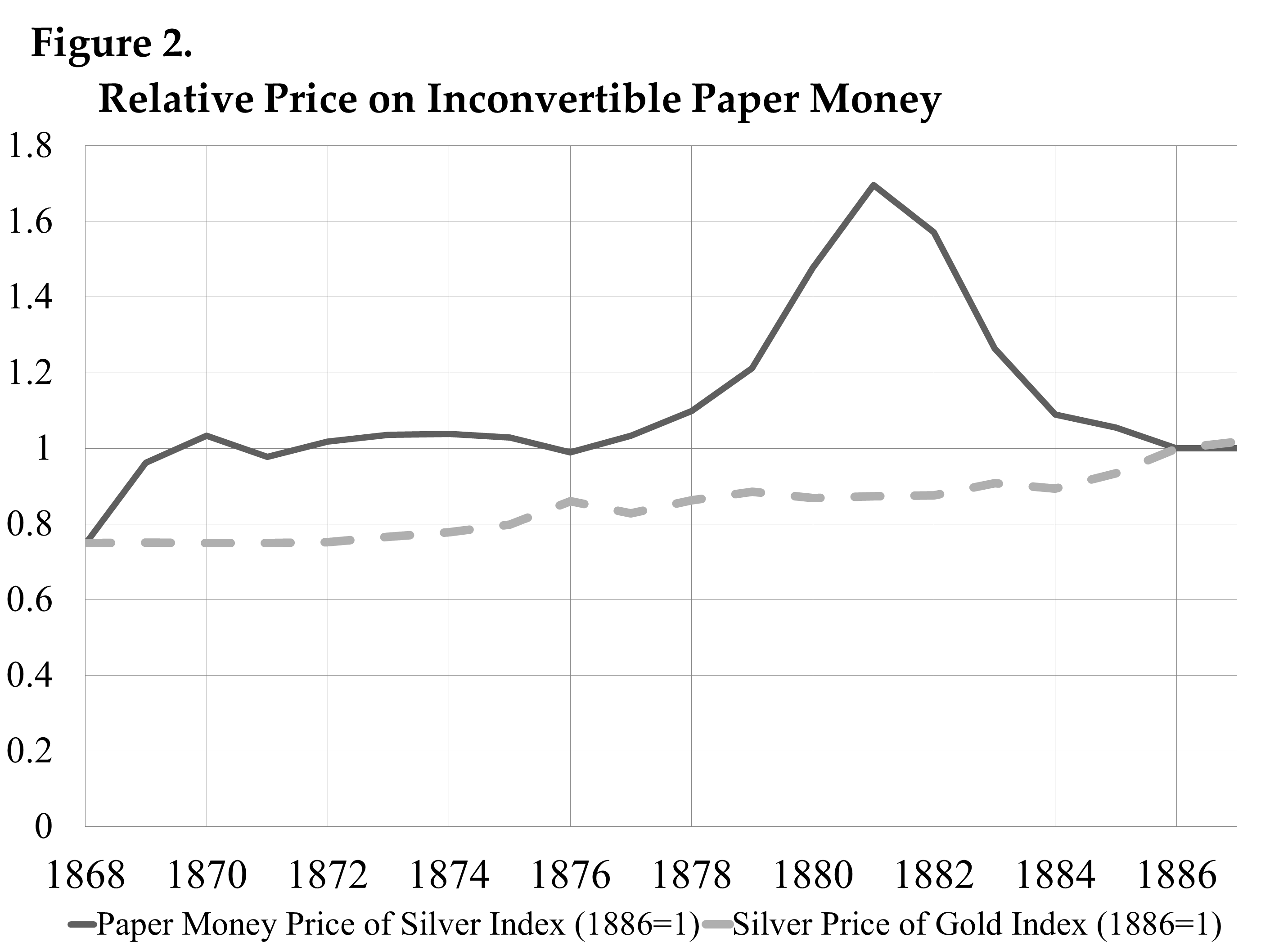

Augmenting the effect of these shocks, in August 1876, the government modified regulations on the nation bank system, abolishing the convertibility of notes, decreasing the reserve requirement, and allowing banks to issue notes against pension bonds deposited with the Treasury. The intended effect was to provide the former samurai with a highly profitable enterprise in which to invest their new bonds—an opportunity they swiftly accepted. Over one hundred national banks were opened by 1880 and a total of ¥34 million notes were issued.[9] The combined impact was dramatic. The infusion of paper money led to a sharp decrease in the ratio of specie to total money supply. The currency system was greatly disturbed, and the balance of payments fell into disequilibrium, generating an outflow of specie. As one would expect, this led to rapid depreciation of inconvertible paper money relative to the price of silver (Fig. 2).

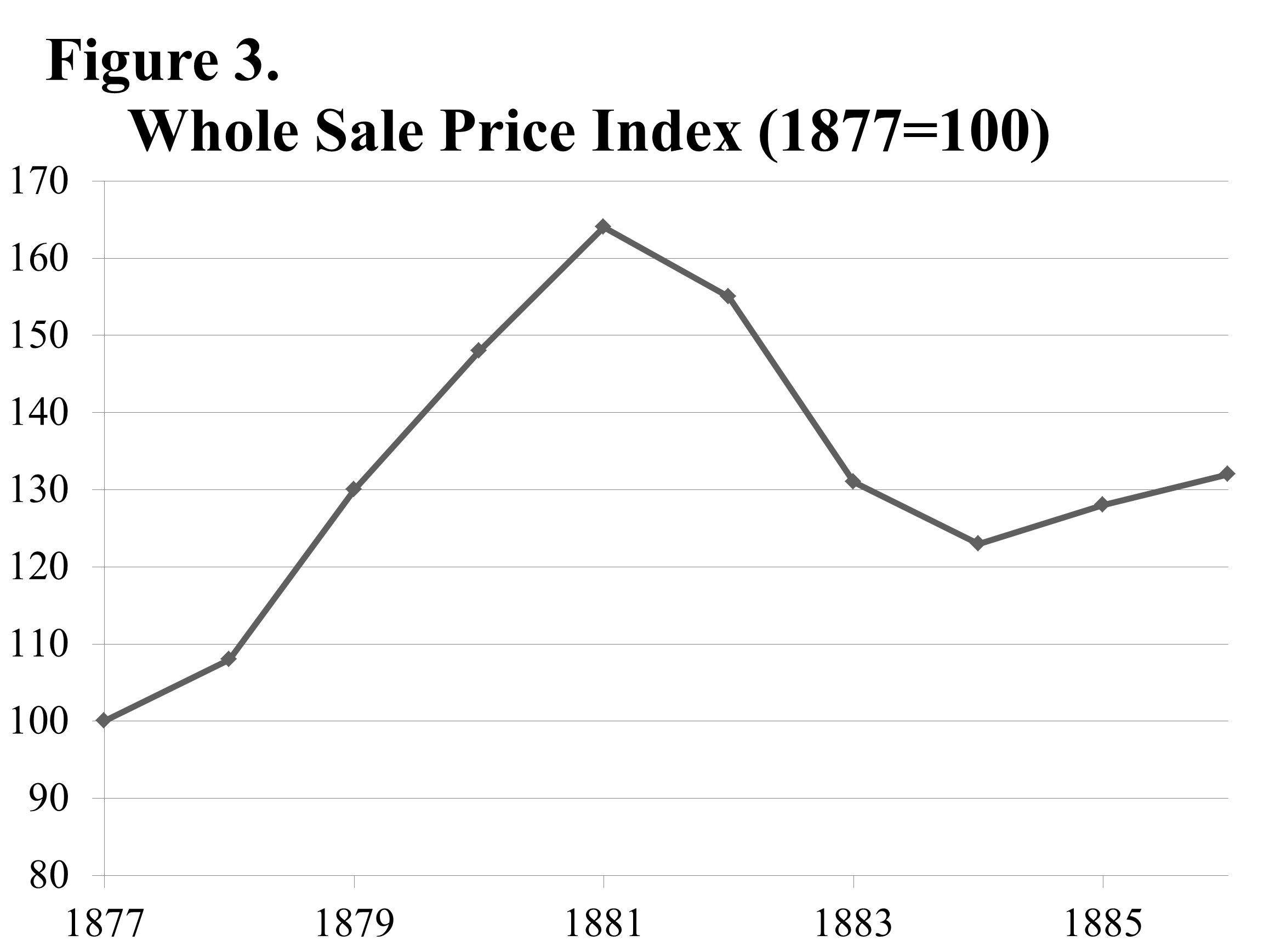

The problem was exacerbated as the Ministry of Finance mistook the depreciation as being due to an insufficient supply of silver. They reacted by issuing coins from the government silvers reserves. These silver coins were either exported or hoarded. The effect was a significant increase in wholesale prices that corresponds to a general rise in inflation (Fig. 3).

Deflationary Policy, 1881-1886

In this disconcerting inflationary environment, Matsukata became Finance Minister. His reaction was to commit the government to budgetary reform, by accelerating a policy already put in place by Ōkuma, which centered on selling government owned factories and retiring the money made in order to contract the money supply.[10] Further, taxes on saké and tobacco were raised, as well as a number of indirect taxes. The surplus was all placed in a sinking fund, pulling large amount of paper notes out of the system. The ratio of specie and convertible notes to total paper money greatly increased, allowing the government to resume convertibility at a low ratio of silver to yen by 1886. Paper money appreciated greatly and the general price level was greatly reduced (Fig. 2 and fig. 3).

In his introduction to the “Report on the Adoption of the Gold Standard,” Matsukata explains that the Government began steps to redeem part of the paper money in circulation as early as September of 1880.[11] Despite being heralded as the engineer of the government retrenchment, he did little in terms of additional concrete steps toward creating a surplus. For example, the increase on the tax of saké was put in place on September 27, 1880.[12] Besides maintaining the previous Finance Minster’s policies, Matsukata also ceased making loans out of the government reserve and pushed for past loans to be paid back to the central government, as well as renegotiated all public bonds to a lower rate of 5%.[13] What set Matsukata’s policies apart from those of the previous finance minister was that they clearly formed part of a larger program “to raise… a sound financial super structure” based on “the establishment of a convertible notes system,” in particular, on the gold standard.[14] One way in which the former minister’s policies were modified in order to fit this larger goal was that the government adopted the policy of using only part of the surplus to redeem paper money, while using the remainder to increase the government’s specie reserve.

That Matsukata saw the adoption of the gold standard as an eventual necessity is clear from his writings. He describes the move toward the de facto silver standard, which was established when the Bank of Japan began issuing convertible notes payable in silver in 1885, as “an inevitable step the country had to take in arriving at last upon financial footing.”[15] He argues that the accumulation of the large gold reserve necessary for the establishment of the gold standard would have been too difficult at the time, necessitating the intermediate step of the de facto silver standard.Nevertheless, even then, it was accepted that in order to achieve “healthy financial development, Japan would have to enter sooner or later the international economic community, and that in order to do this she would have to adopt a gold standard.”[16] On a practical level, the claim that entrance in the international economic community required a gold standard may have been motivated by the fact that the declining price of silver against gold created an unstable exchange rate against gold standard countries. It is likely, however, that Matsukata’s beliefs were deeply influenced by Léon Say, the French Finance Minister, who encouraged the adoption of many financial policies prominent in the West.

Léon Say and a New Path for Financial Policy

In 1878, Matsukata traveled to Europe as a delegate to the International Exhibition in Paris, where Léon Say took Matsukata under his wing.[17] Say was a firm believer in the importance of a sound convertible currency backed by gold and likely advised Matsukata that a gold standard was essential for establishing the state’s credit and respectability in the eyes of international bankers.[18] Say’s influence on Matsukata can also be seen in relation to the transfer from the national bank system to the central bank system, which Matsukata facilitated in 1882 with the establishment of the Bank of Japan. Say is known to have urged Matsukata to shift to a system in which a single central bank would be the sole issuer of notes and has strong control over other banks. This change would ensure that the government would have greater control over the issuing of bank notes, avoiding the influx of new note issues associated with the revised national banking laws of 1876.[19] Matsukata clearly considered Say a significant influence, encouraging the emperor to confer on Say the First Class Order of the Rising Sun, the highest civilian decoration in Japan, in 1883.[20] The idea of using convertibility as signal for influencing perceptions of Japan’s financial condition would prove important in guiding Matsukata’s decisions as Finance Minister.

In 1878, Matsukata traveled to Europe as a delegate to the International Exhibition in Paris, where Léon Say took Matsukata under his wing.[17] Say was a firm believer in the importance of a sound convertible currency backed by gold and likely advised Matsukata that a gold standard was essential for establishing the state’s credit and respectability in the eyes of international bankers.[18] Say’s influence on Matsukata can also be seen in relation to the transfer from the national bank system to the central bank system, which Matsukata facilitated in 1882 with the establishment of the Bank of Japan. Say is known to have urged Matsukata to shift to a system in which a single central bank would be the sole issuer of notes and has strong control over other banks. This change would ensure that the government would have greater control over the issuing of bank notes, avoiding the influx of new note issues associated with the revised national banking laws of 1876.[19] Matsukata clearly considered Say a significant influence, encouraging the emperor to confer on Say the First Class Order of the Rising Sun, the highest civilian decoration in Japan, in 1883.[20] The idea of using convertibility as signal for influencing perceptions of Japan’s financial condition would prove important in guiding Matsukata’s decisions as Finance Minister.

In addition to his firm stance regarding convertibility, Say strongly supported a form of laissez-faire orthodoxy, which discouraged the direct involvement of the government in industrialization.[21] While the Japanese government was already taking steps toward reducing its direct involvement in industry by auctioning off its model-factories and reducing subsidies, Matsukata pursued this policy not simply out of the need to close the deficit and reduce inflation, but as part of a general view of economic policy involving a reduced role for government in enterprise. That Matsukata held this stance is reflected in an 1882 memorandum: “The Government should never attempt to compete with the people in pursuing industry or commerce, for in such matters it can never hope to equal in shrewdness, foresight, and enterprise men who are actuated by the immediate motives of self-interest.”[22]

While Matsukata believed firmly in the noninvolvement of the government in private enterprise, he recognized that the regulation of the currency necessitates intervention. For this role, he advised the creation of a central bank, arguing that “since the Government ought not and can not [sic] engage in commercial enterprise, the only possible course for the government to pursue would be to provide a special organ” to fulfill this role.[23] Essentially, this was a call for the separation of the financial policy from monetary policy. Generally the separation of monetary policy and fiscal policy is, like in the United States today, intended to allow the central bank to pursue its macroeconomic objectives free of political influence. While this idea is evident in Matsukata’s interest in limiting government intervention in industry, there is reason to believe that the monetary policy was not entirely apolitical, as will be discussed in the following sections.

Government Perceptions of Inflation

By establishing convertibility, balancing the budget, and creating a central bank, the Matsukata reforms essentially separated government monetary operations from its fiscal operations, bringing an end to inflation and inducing the government to follow more responsible financial policies. There is reason, however, to question whether inflation was truly such a problem so as to justify these reforms. The price of the rice, which underwent the largest increase between 1877 and 1880, never experienced a year over year percentage increase of more than 25% (Table 1). The overall rate of inflation was most surely under this value, suggesting that inflation never reached an extremely high level. In fact, even Matsukata recognized that the immediate effects of inflation were ostensibly positive, but claimed that the ever increasing prices formed an unsustainable trend as “farmers contracted habits of luxury,” and “the industrial classes became over-excited with vain hopes of speculation.”[24] This comment suggests the Matsukata saw the inflation as part of a speculative bubble and there is evidence to support that such a bubble existed. The price for rice increased at a rate that outstripped the increases in prices for other goods (Table 1). Even in 1879 and 1880, when record harvests occurred, farmers continued to hoard their crop and to take out loans at high interest rates to pay for necessities, anticipating being able to sell it at even higher prices in the future.[25] In early 1881, the central government announced the land tax would be collected earlier in the year, resulting in a rush by farmer to sell hoarded rice to pay off loans and satisfy stricter tax laws, ending the speculative bubble. Thus, the economy was poised for economic downturn before Matsukata’s increased retrenchment policy. The policies of retrenchment and deflation were just the opposite of the Keynesian pump-priming measures needed in order to spur economic recovery (though, obviously, this was prior to the introduction of Keynesianism). In addition, it is likely the case that windfalls to rural landowners had already been reduced by the contraction of the economy, induced by the note retirements, tax increases, and spending cuts that occurred prior to Matsukata’s taking office. Paired with these events was a downturn in the world economy. From this perspective, Matsukata’s policies appear as misguided as that of Inoue, whose deflationary policy in 1930 threatened to throw the Japanese economy into depression.

At the time, however, the central government did not observe any reverse in the inflationary trends, seeing further policies as necessary. Matsukata describes, in 1881, the period during which he took the office of Financial Minister as a “crisis,” saying “the depreciation… continued without a sign of abatement.”[26] In the following year, 1882, the situation was seen as worsening as Matsukata noted the detrimental effect of “the fact that the imports of the country always exceed the exports, causing the ever increasing efflux of specie.”[27] He claimed that the outflow of specie caused a rapid increase in interest rates, which deprived firms of needed capital, greatly reducing investment. An upward trend in interest rates began in 1877, supporting Matsukata’s observations.[28] On the other hand, a report published by the Ministry of Agriculture and Forestry in 1884 lists over a hundred new import substitutes being produced, suggesting that the impact of inflation on industrialization was not particularly damaging.[29] In addition, throughout this period, there was an uninterrupted upward trend in the yearly value of manufacturing production from 800 million to nearly 1,200 million yen.[30] While the high interest rates may have reduced the degree of investment, the statistics do not support the claim the general project of industrialization was threatened. One could conclude from this that the claims regarding the immediate negative effects of inflation were partially rhetoric intended as an excuse for Matsukata to push his more general financial reforms.

Even if one takes as given that he was justified in taking actions toward ending worrisome inflation and signaling greater financial responsibility by eliminating deficit and moving toward convertibility, it remains uncertain as to why the government pushed for a deliberate policy of deflation through the redemption of paper money. Rather than pursuing a deflationary policy, Japan could have established convertibility at a new par by devaluing the yen in terms of specie and limiting the right to issue new notes to the Bank of Japan, which would have allowed the government to stabilize prices without the drop in real output caused by deflation. One answer is to say that it was generally considered improper to adjust the otherwise fixed exchange rates and, thus, would have threatened respectability; however, this response is particularly strong on its own, as such a policy was not without precedent in other countries. On the surface, deflation seemed highly misguided since it was linked to a significant recession in the agricultural sector and it raised the real value of outstanding samurai commutation bonds.

Proposed Motivations for Inducing Deflation

To explain the government’s motivation for inducing deflation, Marxist scholars have offered a number of theories involving political motivation. Perhaps Matsukata intended to undercut the Popular Rights Movement, perhaps he wanted to create a budget surplus for armaments expansion; no evidence exists for these explanations.[31] Another theory, however, suggests a much more plausible motivation for inducing deflation: the need to raise the real value of the land tax receipts. As a result of the fixed land tax that had been instituted, the doubling of the price of rice created enormous profits for landowners, while adversely affecting the government. The real purchasing power of the tax receipts continued to fall, while the government lacked the ability to siphon off any of the landowners profits, other than some insufficient new taxes on tobacco and saké. The problem was only aggravated in 1877 when the nominal tax rate was reduced from 3% to 2.5%, due to riots against the government.[32] Suggestions were made to base the land tax at least partially on the price of rice, but these proposals were rejected. Finance Minister Ōkuma had suggested a foreign loan, but this was opposed, since it was seen as potentially endangering Japan’s independence from European powers. The rejection of this proposal was based on the nationalist concept that Japan needed to establish itself as self-reliant, putting itself alongside nations like Britain and France, rather than allowing it, as Matsukata said in 1881, to “shift and sink to the condition of Egypt, Turkey, or India.”[33] Increasing the nominal tax rate sharply enough to compensate for losses would have likely led to rural discontent. Therefore, the government had few options other than to raise the purchasing power of the tax receipts by instituting deflation. Matsukata viewed the government as having an essential role in guiding the successful growth of the economy. The deflationary policy prevented the government from having to confront the future problem of insufficient revenue, due to decreasing real value tax receipts. This policy was consistent with the establishment of a central bank with a convertible currency, which was also a way of ensuring the government monetary influence.

An alternative explanation seeks to justify the move to convertibility at a lower ratio of paper money to specie as an indirect method of signaling Japan’s wealth to foreign nations. Given the global attitudes toward monetary policy at the time, a government with ability to maintain convertibility of its currency provides a credible signal to other nations that the government holds significant liquid reserves and has adequate fiscal resources that it does not need to resort to inflation to meet its needs.[34] The reason for this is rooted in an analysis of speculators in the market for specie.[35] A speculative attack that exhausts the reserve of a government with a convertible currency forces the price of specie in terms of paper money to be decided freely by market forces. Speculators will only want to conduct such an attack if they suspect that it would cause currency to depreciate relative to specie, raising the price of the precious metals. Before actually exhausting the government reserves, the speculators cannot know for sure whether the attack will cause an increase or a decrease in the price of specie. Thus, the speculators are open to some degree of risk. The larger the government reserves the greater the amount of the speculators’ own wealth that must be used to exhaust the reserves. This implies that the larger the reserves, the more risk the speculator must face. Thus, in order to maintain a convertible currency that is safe from speculative attacks, the government reserve must be large, heightening the speculators’ risk and discouraging an attack. The implication is that a country with a convertible currency must have a large reserve, indicating a significant degree of financial strength. This explanation also provides a reason for creating deflation. Lowering the yen price of silver implies that a larger specie reserve is required to maintain convertibility. Since the supposed goal of the Meiji government was to signal its financial strength in the form of a large government reserve, establishing convertibility at a new par with a smaller reserve would have be less desirable than doing it at the appreciated value of the yen.

One could describe the buildup of specie reserves as a militaristic move, relating the policy to the political rise of Itō Hirobumi in 1881, who favored increased military adventurism and autocratic rule. Strengthening the military and naval forces and producing the latest weapons and ships would require significant investment, and establishing fiscal soundness would provide the government with the means to initiate a military buildup. Convertibility, by signaling to other nations the possession of a large liquid reserve, alerted the international community of Japan’s war chest and their potential to be a military adversary. While this explanation has some credibility, more likely the signal intended for the international community was that Japan had a stable and sound economy, encouraging investment and establishing the government’s credit, agreeing with Minister Say’s advice that a convertible currency is essential for gaining respectability. While not directly militaristic, increasing the reserves established the security of the Japanese economy and discouraged potential imperialist intervention by foreign nations. Referring back to Matsukata’s argument for rejecting the foreign loan, it is clear that he was concerned with Japan’s standing in relation to other countries. The adoption of institutions such as a central bank and convertibility, which were prevalent among Western nations, served as a means of establishing Japan’s place among the developed and powerful nations.

Conclusion

Though in part a move toward curbing what was perceived as rampant inflation, the Matsukata Deflation was an element of a larger restructuring of the Japanese financial and monetary systems. Upon taking the office of Finance Minister in 1881, Matsukata pursued a single-minded program, inspired by Léon Say, aimed at strengthening the government’s financial security, while laying the financial foundation for the growth of the nation’s economy through the establishment of a sound monetary system and a reduced degree of government involvement in industry. The retrenchment and the redemption of paper money served the important purposes of enabling the buildup of a specie reserve that would facilitate the adoption of a gold standard, signaling Japan’s financial security to the international community—a goal that was finally achieved with the establishment on gold convertibility in 1897.

Though reinforcing a painful economic downturn in the agricultural sector, the deflationary policy ensured the government a source of revenue by increasing the value of its land tax receipts, thereby enabling the government to move away from a policy of issuing notes to fund expenditures. On its own, the instigation of deflation would be an unjustifiably harsh method of increasing the real value of the government’s revenue; however, the policy represented part of a coherent program which included the establishment of a central bank system and a balanced budget. Prior to Matsukata’s reforms, the Japanese government pursued a potentially unsustainable financial policy, in which it had insufficient tax revenues and unsupportable burdens due to costly industrial policy and heavy transfer spending. The Matsukata Deflation was one of a set of policies which placed the Japanese government on sound financial footing, separated monetary and financial policy, and signaled to the world Japan’s potential for growth.

[1]Neil Waters, Japan’s Local Pragmatists: The Transition from Bakumatsu to Meiji in the Kawasaki Region, (Cambridge: Harvard University Press, 1983), 104.

[2] Masayoshi Matsukata, Report of the adoption of the gold standard in Japan, (Tokyo: Government Printing Press, 1899) https://archive.org/stream/cu31924021473057, 43.

[3] Henry Rosovsky, “Japan’s Transition to Modern Economic Growth, 1868-1885,” Industrialization in Two Systems, (New York: John Wiley, 1966), 130.

[4] David Flath, The Japanese Economy, (Oxford: Oxford University Press, 2000), p. 30.

[5] Rosovsky, “Japan’s Transition to Modern Economic Growth, 1868-1885,” 127.

[6] Ibid.

[7] Ibid., 129

[8]Koichi Emi and Nobukiyo Takamatsu, “Meiji Iko Zaisei Shushi no Suikei 1868-1929 [Estimated government revenue and expenditure in japan after the Meiji Era 1868-1929],” Kokumin Shotoku Suikei Siryo [The Underlying Data for Estimates of Long Term Economic Statistics of Japan since 1868], (Tokyo: Institute of Economic Research, Hitotsubashi University, 1962).

[9]Rosovsky, “Japan’s Transition to Modern Economic Growth, 1868-1885,” 130.

[10] Matsukata, Report of the adoption of the gold standard in Japan, 39.

[11] Ibid., III

[12] Ibid., 39

[13] Ibid., 41

[14] Ibid., IV

[15] Ibid.

[16] Ibid.

[17] Haru Reischauer Matsukatu, Samurai and Silk: A Japanese and American Heritage, (Cambridge: Belknap Press, 1988), 83.

[18] Rosovsky, “Japan’s Transition to Modern Economic Growth, 1868-1885,” 133.

[19] Matsukata Reischauer, Samurai and Silk, 83.

[20] Ibid., 96.

[21] Matsukata Reischauer, Samurai and Silk, 84.

[22] Matsukata, Report of the adoption of the gold standard in Japan, 54.

[23] Ibid., 55.

[24] Ibid., III.

[25] Ericson Steven, “The Matsukata Deflation and Rural Distress in Mid-Meiji Japan,” New Directions in the Study of Meiji Japan, ed. Helen Hardacare, Adam Kern (Leiden: Brill Academic, 1997), 339.

[26] Matsukata, Report of the adoption of the gold standard in Japan, IV.

[27] Ibid., 43.

[28] Matsukata, Masayoshi. Report of the adoption of the gold standard in Japan, (Tokyo: Government Printing Press, 1899) https://archive.org/stream/cu31924021473057, 29, 98

[29] Rosovsky, “Japan’s Transition to Modern Economic Growth, 1868-1885,” 131.

[30] Ohkawa, Kauhi. Patterns of Japanese Economic Development: A Quantitative Appraisal. (New Haven: Yale University Press, 1979), 302-303.

[31]Ericson, “The Matsukata Deflation and Rural Distress in Mid-Meiji Japan,” 390.

[32]Flath, The Japanese Economy, 32.

[33]Quoted in John H. Sagers, Origins of Japanese Wealth and Power: Reconciling Confucianism and Capitalism, 1830–1885, (New York: Palgrave Macmillan, 2006), 122.

[34]Ibid., 33.

[35]Paul Krugman, and Julio J. Rotemberg, “Speculative Attacks on Target Zones,” Exchange Rate Targets and Currency Bands, ed. Paul Krugman and Marcus Miller (Cambridge: Cambridge University Press, 1991)http://www.hbs.edu/faculty/Pages/item.aspx?num=4969 (accessed November 28, 2013).

Bibliography

Emi, Koichi, and Nobukiyo Takamatsu. Meiji Iko Zaisei Shushi no Suikei 1868-1929 [Estimated government revenue and expenditure in japan after the Meiji Era 1868-1929]. Kokumin Shotoku Suikei Siryo [The Underlying Data for Estimates of Long Term Economic Statistics of Japan since 1868]. Tokyo: Institute of Economic Research, Hitotsubashi University, 1962.

Ericson , Steven. The Matsukata Deflation and Rural Distress in Mid-Meiji Japan. New Directions in the Study of Meiji Japan. Edited by Helen Hardacare, Adam Kern. Leiden: Brill Academic, 1997.

Flath, David. The Japanese Economy. Oxford: Oxford University Press, 2000.

Krugman, Paul, and Julio J. Rotemberg. Speculative Attacks on Target Zones. Exchange Rate Targets and Currency Bands. Edited by Paul Krugman and Marcus Miller. Cambridge: Cambridge University Press, 1991. http://www.hbs.edu/faculty/Pages/item.aspx?num=4969 (accessed November 28, 2013).

Matsukata , Masayoshi . Report of the adoption of the gold standard in Japan. Tokyo: Government Printing Press, 1899. https://archive.org/stream/cu31924021473057.

Patterns of Japanese Economic Development: A Quantitative Appraisal. Edited by Kazushi Ohkawa; Miyohei Shinohara; Larry Meissner. New Haven: Yale University Press, 1979.

Reischauer Matsukatu, Haru. Samurai and Silk: A Japanese and American Heritage. Cambridge: Belknap Press, 1988.

Rosovsky , Henry. Japan’s Transition to Modern Economic Growth, 1868-1885. Industrialization in Two Systems. Edited by Henry Rosovsky. New York: John Wiley, 1966.

Sagers, John H. Origins of Japanese Wealth and Power: Reconciling Confucianism and Capitalism, 1830–1885. New York: Palgrave Macmillan, 2006.

Tsuru, Shigeto. Essays on Japanese Economy. Tokyo: Kinokuniya, 1958.

Waters, Neil. Japan’s Local Pragmatists: The Transition from Bakumatsu to Meiji in the Kawasaki Region. Cambridge: Harvard University Press, 1983.

Leave a Reply